|

Planned

Value (PV):

Example:

we have an 8 week activity with a 10KCHF budget linearly distributed.

After 2 weeks, we have PV=10KCHF*2/8=2.5 KCHF.

The

portion of work expected to be completed at a given date,

times the authorized budget allocted to carry out that work.

Amount of work scheduled measured as an estimation in CHF.

In former project management jargon, it is the budgeted

cost of work scheduled (BCWS).

Earned

Value (EV):

Example:

If the 8 week activity consists at manufacturing and delivering

10 magnets (linearly distributed), then when the 6 magnets

are delivered: EV=10kCHF*6/10=6 kCHF.

The

value of completed work expressed in terms of the budget assigned

to that work.

Actual

Cost (AC):

Example:

If when statusing you have paid 7 kCHF, these are your actual

costs.

The

costs actually incurred and recorded in accomplishing the

work performed.

Budget

at completion:

The total authorized budget for accomplishing the program

scope of the work. In other words, it is the sum of the planned

values at completion of the project.

|

Pre-requisites

to setting up an EVM system

A

clear scope of work is a pre-requisite for setting up

such a system. A WBS (Work Breakdown Structure) is probably

the best mean for doing so.

The

WBS is a structured list of all the activities to carry

out in order to complete a project. For each single

activity, all the resources required (material, manpower,

overheads...) must be identified and quantified. Allocated

budgets should be based on these estimates. Short term

activities are easier to estimate and schedule than

long term activities; therefore EVM standards allow

that long term activities remain agregated in planned

packages with unallocated budgets.

|

|

|

The

performance of the project, or sub-project, or of a

single activity is measured using few indices:

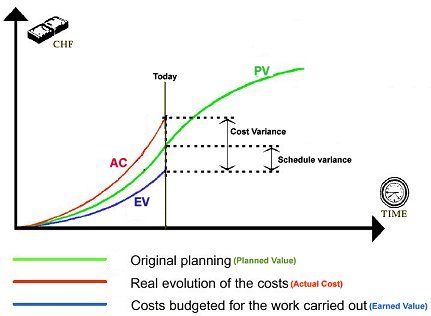

Schedule

variance (SV):

compares the actual physical progress (EV) to the planned

one (PV): SV=EV-PV

If SV is negative, this means that the activity is behind

schedule.

If SV is positive, the activity is ahead of schedule.

Example:

Using previous example, if 6 magnets are delivered at

the end of week 6, then EV=6 kCHF and PV=7.5kCHF, then

SV= -1.5kCHF

Cost

variance (CV):

compares the actual costs (AC) to the actual physical

progress, i.e the earned value (EV):.

CV=EV-AC

If CV is negative, this means that the budget tends

to be overrun

If CV is positive, the budget tends to be underrun.

Using previous example, let's

statusing at end of week 6:

at that date, PV = 10 kCHF × 6/8 = 7.5 kCHF

if 6 magnets are delivered at the end of week 6: EV

= 10 kCHF × 6/10 = 6 kCHF

if incurred expenditures are 7 kCHF, then AC = 7 kCHF.

SV

= 6 kCHF - 7.5 kCHF = -1.5 kCHF < 0 activity is behind

schedule.

CV = 6 kCHF - 7 kCHF = -1 kCHF < 0 the budget is being

overrun!

|

|